BOC Kenya PLC (NSE: BOC) – Equity Research (29 May 2026)

- May 29

- 7 min read

Executive Summary

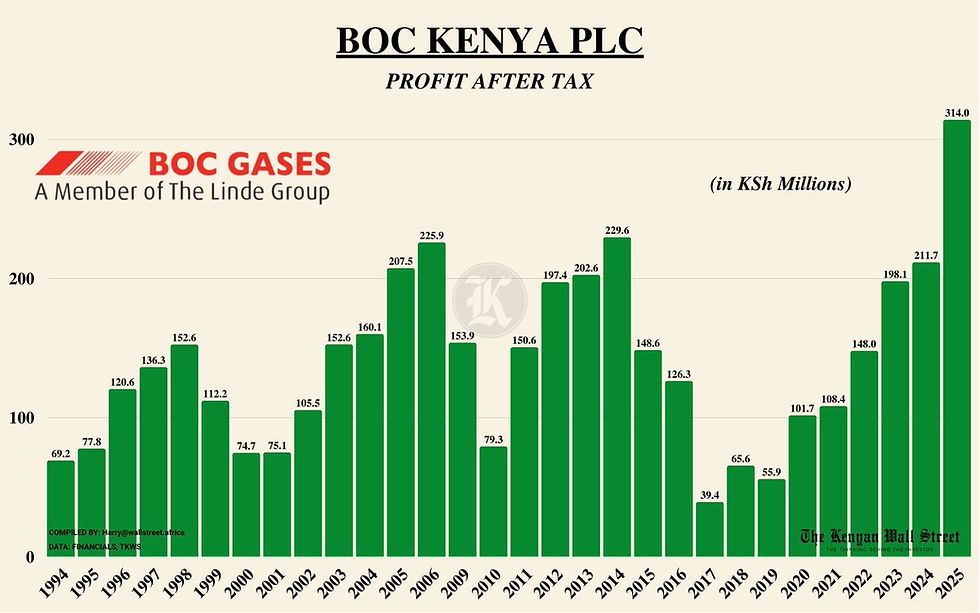

BOC Kenya is a niche supplier of industrial and medical gases in East Africa, leveraged to both healthcare (defensive) and industrial demand. In FY2025 it delivered strong growth – Revenue +18.5% to KES 1.427bn, Net Profit +48.4% to KES 314.0m (EPS KES 16.08) – driven by post-pandemic medical gas de

mand and engineering projects. The Board proposes a total dividend of KES 12.85/share (80% payout). However, the stock now yields only ~7.3% (KES12.85/176) at ~KES176, well below Kenya’s ~12% 10Y government bond yield. This implies investors are pricing in further growth or a sharp drop in rates. Our analysis confirms BOC is a stable, cash-generative business with high barriers (own facilities, long-term contracts), but largely mature and sensitive to Kenya’s macro (energy costs, inflation, FX). We find fair-value estimates roughly in the KES165–185 range: under reasonable DDM/DCFM assumptions the current KES176 price is near fair, but offers only limited upside. We therefore issue a HOLD recommendation for most investors. Income-focused shareholders have a well-covered dividend (supported by strong cash flow), but new buyers are paying a full valuation. Key catalysts will be continuation of healthcare/industrial demand and stable energy prices; risks include tightening policy, cost inflation and liquidity constraints in a small free float.

Key Thesis:

Stable, niche business: BOC dominates Kenya’s industrial/medical gas market (oxygen, nitrogen, LPG, welding gases) with long-term contracts and capital-intensive infrastructure. Medical oxygen (for hospitals) provides a defensive base, while industrial gases (welding, food processing etc.) are cyclical.

Recent performance: FY2025 revenue KES1.427bn (+18.5% YoY) and PAT KES314.0m (+48.4% YoY), with EPS KES16.08 and dividend KES12.85. Profit margin reached ~22%. Growth was driven by price adjustments and project roll-offs. This followed a 2024 revenue decline (–22% vs 2023), so recent growth partly reverts earlier weakness.

Dividend and yield: BOC’s high payout (~80%) makes it “bond-like” for income investors. The 2025 dividend yield (~7.3% gross) is below Kenya’s 10-year bond (~12%) and below top local dividend stocks, implying the stock trades like a low-yield equity.

Valuation: Our DDM and DCF models (assuming KES12.85 DPS, modest 5–7% growth and ~12% discount) yield a fair range roughly KES160–190. For example, at k=12%, g=5% we get ~KES193; at g=4% ~KES167. A DCF on net profit projects ~KES177 (base case). This is in line with current KES176. Earlier “ultra-conservative” DCF targets (~KES117.74) seem too low given steady cash flows. The stock appears roughly fairly valued at ~KES176 under normal growth; only a bear scenario (sluggish growth, high rates) justifies a large discount.

Macro environment: Kenya’s economy is moderate growth but with rising inflation. Headline CPI hit ~6% in May 2026 (driven by fuel/food costs) and 10Y bond yields are ~12%. BOC’s costs (electricity, transport) have been rising. High rates make its ~7% yield less attractive. Unless inflation moderates or rates fall, investors require solid growth to compensate.

Sentiment/Liquidity: BOC is lightly traded (market cap ~KES2.5bn, float ~35%). It was up ~78% in the last year amid limited analyst coverage. This suggests a scarcity premium and retail momentum. There’s no evident new takeover – a prior Carbacid bid was withdrawn – but investor interest remains on any strategic news.

Collectively, BOC is not a cheap growth stock – it’s valued as a defensive yield play. The current price assumes stable dividends and modest growth; upside requires better-than-expected demand or lower rates. Downside is capped by the high dividend floor, but could occur if the economy weakens or inflation spikes. We see no clear undervaluation or fresh catalyst, thus a neutral stance.

What the Market May Be Pricing In

At ~KES176, BOC is trading at a peak multiple relative to its defensive peers and government securities. The sub-8% dividend yield is well below Kenya’s risk-free rate (~12% for 10y bonds), implying the market expects either sustained strong growth or falling rates. Given ~6–7% inflation and rising energy costs, it seems more likely investors are treating BOC as a bond proxy: they accept a lower yield in exchange for stable cash flow. In other words, the stock price largely reflects a steady-stream scenario (flat/dividends plus modest 4–6% growth). Any forecast beyond moderate growth would already be built in. The stock’s 1-year gain (+78%) suggests faith in continued recovery after the 2024 slump and confidence in the dividend. It may also reflect a “scarcity premium” – BOC’s 65%-held by Linde, small float, and few direct comparables allow big price swings with limited volume (as noted by Simply Wall St’s volatility flag).

Investor expectations likely include: uninterrupted dividend hikes and more industrial/healthcare contracts. Conversely, any sign of margin pressure (from cheaper competitor entry or unpassed cost inflation) or a policy-rate surprise could quickly reverse sentiment. Currently, with analysts scarce, BOC’s pricing implies its future earnings roughly match or slightly beat moderate-growth models (our base-case DCF yields ~KES177).

Bull / Base / Bear Cases

Bull Case: Stronger economy or healthcare demand. If Kenya’s capex and construction rebound, and hospital expansions continue, both industrial and medical gas sales could exceed our forecasts. BOC could ramp up specialty projects (e.g. liquid oxygen pipelines) or win new contracts in neighboring East African markets (Uganda/Tanzania subsidiaries). Coupled with a decline in power tariffs or fuel costs, margins would improve. In this case, EPS might grow >10% p.a., allowing the payout to rise faster than our 4–6% assumption. The stock could re-rate, targeting a higher P/E (~15x) or ~14% yield – implying a 12-month target > KES190–200. Positive surprises or M&A activity (e.g. new Linde investments) could be catalysts.

Base Case: Stable, defensive income. We assume Kenya’s GDP grows modestly (~4–5%) and inflation stays ~5–7%. BOC maintains volume/pricing growth in line with national demand (c.5–6% long-term). Costs (electricity, fuel) continue rising, but BOC largely passes them through. Dividend grows 5% p.a. (DPS→KES13.5 in 2026, 14.2 in 2027, etc.), keeping yield 7%. Under this scenario, DCF (k12%, g2%) gives fair value KES170–180, and DDM (k12%, g5%) ~KES168–193. The current price ~KES176 sits near mid-range. We forecast a 12-month target of ~KES180 (±10% band), i.e. little to modest upside. Returns will mainly be the dividend, with price gains only if macro easing occurs.

Bear Case: Economic/operational headwinds. If Kenya enters a slowdown or double-digit inflation, industrial gas demand could stall. Elevated energy costs might eat into margins if BOC cannot fully pass them on (contracts may limit price hikes). Further, higher CBK policy rates (to tame inflation) would push interest rates above 12%, making equities like BOC less attractive. A severe scenario: margin falls to historic lows, dividend growth stalls or is cut, and investors demand a yield >10%. Then DCF fair value might drop toward KES120–140. The stock could fall back towards the ~KES100–120 range (support seen in 2024), especially if global uncertainties curb investment. However, even in this case the relatively high dividend and net cash would cap losses around the payout floor.

Key Risks

Commodity/Energy Inflation: BOC’s production is power- and fuel-intensive. Surging electricity or fuel costs (e.g. due to Middle East conflict) could pressure margins if not passed fully to customers.

Macro slowdown: A weak Kenyan economy (e.g. from tightening monetary policy or currency crisis) would reduce industrial demand. FY2024 showed how sensitivity to local capex can cut revenue. Healthcare demand may soften if public budgets shrink.

Interest-rate regime: If CBK keeps rates elevated beyond current levels, the equity risk premium demanded by investors rises. A higher discount rate would lower fair value (e.g. 14% vs 12% cost-of-capital markedly cuts valuations).

Currency/FX: BOC imports some equipment/gases. A sharp KES depreciation raises import costs, potentially squeezing profits if contracts are KES-based.

Competition & regulation: While BOC has barriers to entry, specialty gas imports or new entrants in industrial gases (or a change in regulatory environment for gas utilities) could erode pricing power over time.

Liquidity & corporate action risk: With ~34% free float and limited analyst coverage, the stock can be volatile. The past Carbacid takeover saga (bid lapsed) shows minority shareholders may be under-, or over-valued, and regulatory uncertainties (like the Capital Markets Tribunal case) can weigh on sentiment.

Dividend sustainability: Although covered by earnings and cash flow, an unexpected drop in profit or aggressive re-investment (e.g. for new plants) might constrain dividend growth. The high payout (80%) leaves little buffer for cuts if profits dip.

Final Verdict

From a retail investor perspective: BOC’s stable market position and hefty dividend make it attractive for income, but the current price appears fairly full. We rate it a HOLD overall.

New Buyer: We see limited upside at ~KES176. Unless one expects a surprising positive development (e.g. major new contract or sudden rate cut), better value may lie elsewhere. The stock’s current yield (~7.3%) is well below fixed-income alternatives (10Y bonds ~12%). We would wait for a pullback (e.g. due to weaker results or broader selloff) or a more compelling entry (yield >9%).

Current Holder (low cost): If you own BOC from much lower prices, the position has done well. Given BOC’s strong coverage and net cash, holding for dividends is reasonable. However, with the valuation near 52-week highs, it would be prudent to trim or sell part of your position and re-allocate if needed.

Income-focused Investor: BOC will continue to pay a high dividend, rising modestly if earnings hold. For an income portfolio, it’s a relatively safe payer (like a mini utility). But note the yield shortfall versus bonds. You’re essentially taking on equity risk for a mid-single-digit yield. Unless interest rates fall, the upside is limited to dividend returns.

Catalysts: Continued government/healthcare investment in oxygen infrastructure and industrial expansion would support the business. Any loosening in Kenya’s rate cycle or decline in energy costs would likely boost the share price (as bond yields fall, stock yields become more attractive). Conversely, rising local interest rates, stalled projects, or margin pressure (from electricity/fuel inflation) could push the stock down. New regulatory or strategic actions by parent Linde (e.g. asset swaps in Africa) could also surprise.

We assign moderate confidence to this view (~60%). A lower-than-expected inflation path or strong new order backlog could make us more bullish; a sudden macro shock or costs spike would lower fair value and force a downgrade.

Recommendation: HOLD (neutral) – the shares should be considered for income but not as deep value.

Comments